Are you wondering if you or your loved ones are fully protected under the Affordable Care Act (ACA)? It’s important to know exactly who is covered—and more importantly, who isn’t.

Understanding these details can save you from unexpected medical bills and help you make smarter health decisions. Keep reading to discover if you fall into one of the groups left out by the ACA and what that means for your health coverage options.

This knowledge could change how you plan for your healthcare needs.

Credit: www.kff.org

Aca Coverage Basics

The Affordable Care Act (ACA) changed how many people get health insurance. It set rules for coverage and help for millions. But not everyone is covered under the ACA. Understanding who qualifies and what plans are covered is key.

This section explains the basics of ACA coverage. It helps you know who can get insurance and what types of plans are available.

Who Qualifies For Aca

Most U.S. citizens and legal residents can use the ACA marketplace. People without other affordable coverage often qualify. Those who earn between 100% and 400% of the federal poverty level get help paying. Some states expanded Medicaid to cover more low-income adults. But not everyone meets these rules. Undocumented immigrants and some short-term visitors are not covered. Also, people with access to employer insurance may not qualify for subsidies.

Types Of Covered Plans

The ACA offers four main plan categories. Bronze plans cover about 60% of medical costs. Silver plans cover around 70% and often get extra help. Gold plans cover about 80%, and Platinum covers 90%. Each plan has different monthly costs and out-of-pocket expenses. All plans cover essential health benefits like doctor visits and prescriptions. Preventive care is included without extra cost. Understanding these plans helps you choose the best fit for your needs and budget.

Undocumented Immigrants

Undocumented immigrants live in the United States without official permission. They face many challenges, especially in accessing healthcare. The Affordable Care Act (ACA) offers health insurance options to many people. Yet, undocumented immigrants do not qualify for these benefits. This section explains why and explores other healthcare choices available to them.

Exclusion From Aca Benefits

The ACA does not cover undocumented immigrants. They cannot buy insurance through the ACA marketplace. They are also ineligible for Medicaid and Medicare under ACA rules. This leaves a large group without access to affordable health plans. The law strictly limits benefits to U.S. citizens and legal residents. This policy affects millions of people living in the country.

Alternative Healthcare Options

Undocumented immigrants can still find some healthcare options. Community health centers offer low-cost or free care. These centers provide basic services like check-ups and vaccinations. Some states run programs that help with emergency care. Many also rely on nonprofit clinics for medical attention. These options do not require proof of legal status.

Short-term Health Plans

Short-term health plans offer temporary coverage for people in transition. They are popular for those who need insurance quickly and for a short period. Many choose these plans during job changes or waiting for other coverage to start.

These plans are not part of the Affordable Care Act (ACA). They work differently from ACA-approved plans and have limits. Understanding these differences helps to make better insurance choices.

Why They Aren’t Aca Compliant

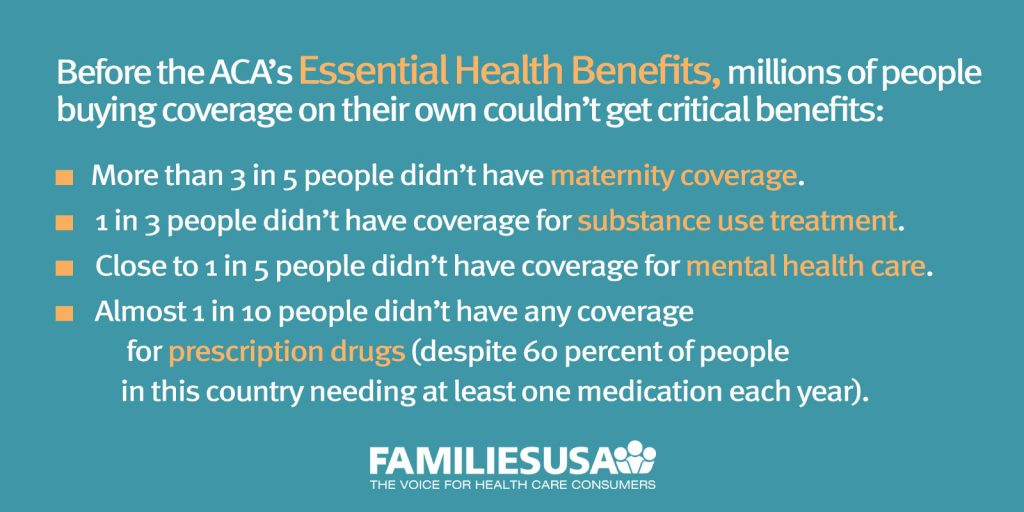

Short-term health plans do not meet ACA rules. They do not have to cover all essential health benefits. There is no requirement to cover pre-existing conditions. These plans can deny coverage based on health status. They often exclude maternity, mental health, and prescription drugs.

ACA plans must follow strict guidelines. Short-term plans avoid these rules to offer lower premiums. This trade-off means fewer protections for enrollees.

Risks And Limitations

Short-term plans often have many coverage gaps. They can end coverage early or refuse to renew it. Medical bills can become very high if serious illness occurs. These plans usually have higher out-of-pocket costs. They may not cover doctor visits or hospital stays fully.

People using short-term plans risk unexpected costs. They might face denial of claims or limited benefits. These risks make short-term plans less reliable for long-term health needs.

Credit: familiesusa.org

Employer-sponsored Plans Exemptions

Employer-sponsored plans have special rules under the Affordable Care Act (ACA). Not all workers with these plans are covered by the ACA’s requirements. Some employers and their workers are exempt. Understanding these exemptions helps clarify who must follow the ACA and who does not.

Small Employers And Coverage

Employers with fewer than 50 full-time workers often have exemptions. These small employers usually do not have to offer health insurance. The ACA mainly targets larger companies. Small businesses can choose to provide coverage but are not forced by the law.

Workers at small companies may not get benefits from ACA rules. They might need to find health insurance through other sources. This exemption helps small businesses avoid heavy costs.

Affordable Coverage Criteria

Large employers must offer affordable health plans to full-time workers. Affordable means the cost is not too high for employees. If the plan costs too much, the employer might face penalties.

Plans must also cover essential health benefits. If an employer’s plan is affordable and meets these benefits, the workers are considered covered under the ACA. Workers in these plans are not eligible for subsidies on the health exchange.

Medicare And Medicaid Differences

Medicare and Medicaid are two major government health programs. They serve different groups of people. Both programs differ from the Affordable Care Act (ACA) in many ways. Understanding their differences helps clarify who is not covered by the ACA.

Overlap With Aca

Medicare mainly covers people aged 65 and older. It also covers some younger people with disabilities. The ACA does not replace Medicare. Many Medicare recipients still use ACA benefits, like prescription drug coverage.

Medicaid serves low-income individuals and families. The ACA expanded Medicaid in many states. This expansion helped many people get coverage. But Medicaid rules vary by state. Some states did not expand Medicaid.

Eligibility Gaps

Medicare eligibility is mostly age-based or disability-based. The ACA covers many people without Medicare. But not everyone fits into these groups. Some low-income adults fall into a coverage gap.

This gap happens in states without Medicaid expansion. People earn too much for Medicaid but not enough for ACA subsidies. These individuals often remain uninsured. They are not covered by Medicare, Medicaid, or ACA.

Non-citizen Residents

Non-citizen residents in the United States face different rules under the Affordable Care Act (ACA). Their eligibility for coverage depends on their immigration status. Many do not qualify for ACA benefits or subsidies. Understanding these rules helps clarify who can use ACA programs.

Legal Status Impact

Legal status determines ACA coverage eligibility. Lawful permanent residents may qualify after five years of residency. Undocumented immigrants cannot get ACA coverage or subsidies. Some visa holders also face limits. The government uses legal status to decide access to healthcare benefits.

State-specific Variations

States have different rules for non-citizen residents. Some states offer Medicaid or state programs to certain immigrants. Others restrict coverage based on federal rules. These variations affect healthcare access. Knowing your state’s policies is important for non-citizen residents.

Religious Exemptions

Religious exemptions are specific rules in the Affordable Care Act (ACA). They allow some people to avoid health insurance requirements. These exemptions protect individuals whose beliefs conflict with buying health coverage. Understanding these exemptions helps clarify who is not covered under the ACA.

Groups With Coverage Waivers

Certain religious groups receive waivers from the ACA coverage rules. These groups refuse health insurance for reasons tied to faith. For example, members of some religious sects do not use insurance at all. They rely on their community and faith for health care needs. The government recognizes these beliefs and offers exemptions.

Implications For Members

People in these groups do not pay penalties for lacking coverage. They do not have to buy insurance or use marketplace plans. However, they may face higher costs if they need medical care. They also might miss out on some health benefits. Still, their religious beliefs guide their health decisions.

Special Cases And Exceptions

The Affordable Care Act (ACA) covers many people, but not everyone fits the rules. Some groups have special cases or exceptions. These exceptions mean some people do not have to follow the usual ACA rules or may not get coverage through it. Understanding these special cases helps clarify who is not covered.

Tribal Members

American Indian and Alaska Native people have unique healthcare options. They can get services from Indian Health Service (IHS) facilities. Tribal members may not need to buy health insurance through the ACA marketplace. They often receive care through tribal health programs instead. This exception respects their special government-to-government relationship.

Other Unique Situations

Some people live outside the U.S. for long periods and may not qualify for ACA coverage. Certain immigrants without legal status also do not qualify for ACA benefits. Members of some religious groups who reject insurance can apply for an exemption. These exceptions address different life situations that the ACA cannot cover.

Credit: www.kidneyfund.org

Frequently Asked Questions

Who Is Excluded From Affordable Care Act Coverage?

Certain groups like undocumented immigrants and some Native Americans may not be covered under the ACA. Also, some short-term or limited benefit plans are excluded.

Are Undocumented Immigrants Covered By The Aca?

No, undocumented immigrants generally do not qualify for ACA coverage or subsidies. They must seek alternative insurance options.

Does The Aca Cover Short-term Health Plans?

No, short-term health plans are not considered minimum essential coverage under the ACA. They do not meet ACA standards.

Are Native Americans Fully Covered By The Aca?

Many Native Americans qualify for special provisions, but some tribal members may face coverage gaps under the ACA.

Conclusion

Not everyone qualifies for coverage under the Affordable Care Act. Some groups, like certain immigrants and people with specific job-based plans, might not be covered. It’s important to know these gaps to find the right health insurance. Understanding who is excluded helps avoid surprises later.

Always check your options carefully. Health coverage matters for everyone’s well-being. Stay informed and plan ahead for your health needs.